Sammaan Capital Ltd is a significant player in India’s non-bank financial company (NBFC) landscape, especially focused on residential mortgages, loans against property and affordable-housing credit. Having re-branded from Indiabulls Housing Finance in 2024, the company is aiming to shed past baggage and reposition itself for growth in a changing credit market. The purpose of this article is to analyse its fundamentals, recent performance and lay out plausible share-price paths over the upcoming decades.

Company Overview

Background

- Incorporated in May 2005 as Indiabulls Housing Finance Ltd, the company later adopted the name Sammaan Capital Ltd in mid-2024.

- Headquartered in India with a network of branches and digital/distribution channels.

- Operates in the housing-finance / mortgage-finance sector, regulated under RBI’s NBFC rules.

Business Model

- Core business: Home loans, loans against property (LAP), affordable housing credit and related secured lending.

- Revenue derives mainly from interest on loans, fee income from allied services and co-lending/assignment arrangements with banks.

- Strategic shift: Moving away from legacy large wholesale exposure, ramping up retail and affordable housing portfolios; enhancing digital sourcing and branch plus channel outreach.

- Distribution/fee income: Cross-selling of insurance, property-related finance products adds to non-interest income streams.

Market Position & Recent Snapshot

| Metric | Details |

|---|---|

| Company Name | Sammaan Capital Ltd |

| Industry | Financial Services / Non-Bank Lending (Mortgage/Affordable Housing) |

| Listed On | NSE: SAMMAANCAP |

| Incorporation | 10 May 2005 |

| Key Change | Name changed from Indiabulls Housing to Sammaan Capital in 2024 |

| Business Focus | Retail mortgages, LAP, affordable housing credit |

Note: specific market-cap and revenue figures vary with time; readers should check the latest filings for up-to-date numbers.

Financial Performance

Here’s a summary of how Sammaan Capital has been performing:

| Year | Revenue / Total Income* | Net Profit/(Loss) | Key Notes |

|---|---|---|---|

| FY2023-24 | ~ ₹8,625 crore | ₹1,214 crore profit | Strong capitalisation, decent asset quality |

| FY2024-25 | ~ ₹8,623 crore (flat) | ~ –₹1,807 crore loss | Major shift in business mix; operating expenses surged |

| Q4 FY25 | Revenue up modestly, Profit ~₹324 crore (quarter) | — | Legacy portfolio reduction, growth, AUM rising |

* Figures rounded; some include total revenues, others operations income.

Key takeaways:

- The company posted a healthy profit in FY24, but FY25 saw a sharp swing into loss territory, largely due to transformation costs, higher expenses and strategic realignment.

- Asset quality has improved in recent quarters (decline in Gross NPAs, reduction of legacy book) and gearing has been brought down significantly.

- The shift toward more retail/affordable housing and away from large wholesale exposures is underway — this is a positive from a long-term risk management perspective.

Key Growth Factors

- Affordable housing boom: With India’s middle class expanding and home-ownership aspirations rising, credit demand in semi-urban and tier-II/III towns is set to grow.

- Strengthening balance sheet: Sammaan’s focus on reducing legacy exposures, improving capital adequacy and lowering leverage helps set the stage for stable future growth.

- Digital and branch expansion: By enhancing its distribution footprint plus digital sourcing, Sammaan can scale lending more efficiently across geographies.

- Co-lending/partnerships with banks: These relationships let Sammaan leverage banks’ balance sheets and reach while sharing risk — valuable in a tighter regulatory environment.

- Cross-selling and fee income: Offering insurance, property-finance add-ons, and ancillary services helps diversify income beyond interest margin.

Risks and Challenges

- Profitability volatility: The transition has led to losses recently — the company must convert growth into sustainable profits.

- Asset-quality risk: Despite improvements, the legacy book and macro headwinds (e.g., real-estate slowdown, interest-rate pressure) remain risks.

- Competitive pressures: Many NBFCs and banks are targeting the mortgage/affordable-housing segment; maintaining margin will be tough.

- Regulatory & funding risk: As an NBFC, changes in regulation (e.g., on leverage, capital adequacy) or access to funding (bonds, NCDs) could impact operations.

- Execution risk: Scaling branch/digital operations in tier-III/IV areas is difficult; cost control and credit discipline will be critical.

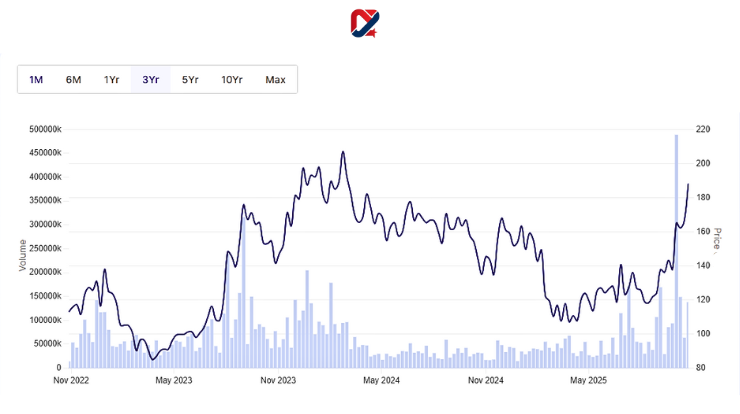

Sammaan Capital Share Price Target

Here are three possible price paths, assuming the company executes well, moderately, or weakly. These are purely hypothetical for educational purposes.

| Year | Bear Case | Base Case | Bull Case | Key Assumptions |

|---|---|---|---|---|

| 2026 | ₹40 | ₹60 | ₹90 | Moderate growth in mortgage business, stable margins |

| 2027 | ₹55 | ₹85 | ₹130 | Affordable-housing portfolio picks up, leverage improves |

| 2028 | ₹70 | ₹110 | ₹170 | Strong mix shift, fee income rising, asset-quality improvement |

| 2030 | ₹100 | ₹160 | ₹250 | Leadership position in semi-urban housing finance, cost efficient |

| 2040 | ₹140 | ₹260 | ₹400 | Diversified finance business, expanded product suite across India |

| 2050 | ₹300 | ₹550 | ₹950 | Full-fledged finance ecosystem, pan-India strong brand, tech-driven growth |

CAGR Expectations:

- Base case: If going from say ₹60 in 2026 to ₹160 in 2030 → ~ ≈ 25%-30% p.a.

- Bull case: From ₹90 in 2026 to ₹400 in 2040 → significant multi-decade growth potential.

Again: These are educational estimates, not a guarantee of future returns.

Expert Opinions and Market Sentiment

Market commentary suggests that Sammaan Capital is undergoing a reset. The reduction of the legacy book and ramp-up of the retail/affordable housing segment are seen as positives. The backing of strong capital, improved governance and a leaner model has improved sentiment. However, many analysts caution that until consistent profitability returns and growth becomes visible, risks remain.

Future Outlook

Looking ahead:

- If Sammaan Capital can consistently grow its affordable-housing loan book and maintain tight credit control, the growth runway is substantial given India’s low mortgage penetration.

- The company’s narrowing legacy exposures and improved capital/leverage make it better positioned than before.

- Key monitoring points for investors: growth rate of the new credit book, margin trends, NPA levels, cost of funds and regulatory changes.

- If the company successfully diversifies beyond just housing (e.g., broader retail credit, gold/personal loans, MSME finance) and executes well, the upside may be significant — provided execution risk is managed.

FAQs

What does Sammaan Capital Ltd do?

It is a non-bank financial company in India that offers home loans, loans against property and affordable housing finance, primarily targeting retail borrowers and lower-to-middle income segments.

Who owns Sammaan Capital Ltd?

It was formerly Indiabulls Housing Finance Ltd and in 2024/25 rebranded as Sammaan Capital. It remains a publicly listed company in India. Major investors and promoters have changed over time.

Is Sammaan Capital a good long-term investment?

It has potential, thanks to growth in housing finance and its business reset, but carries higher risk due to past issues, profitability volatility and execution challenges. A long-term investor should weigh both the upside and the risks.

What is the Sammaan Capital share price target for 2030?

In the base scenario, I’ve estimated around ₹160 by 2030; in a bull scenario, around ₹250. These are hypotheticals, not guaranteed.

What was the relationship between Sammaan Capital and Indiabulls Housing Finance?

Sammaan Capital is the rebranded name of Indiabulls Housing Finance Ltd. The business and legal entity transformed, signalling a fresh chapter and strategy shift in the same business framework.

Conclusion

Sammaan Capital Ltd is at an inflexion point: from legacy issues and a heavy wholesale/wholesale exposure model, it is moving toward retail-focused, affordable-housing financing, with a stronger capital base and better risk metrics. The potential for long-term growth exists, especially as India’s credit and housing markets evolve — but the journey is far from certain. The share-price targets laid out here (bear, base, bull) illustrate what could happen under different scenarios. If you’re considering investing, dive into the quarterly disclosures, monitor execution, keep the long horizon in mind and prepare for variability. Stay curious, stay measured and keep doing your research.